Why Your Total Addressable Market Is Different (Bigger) Than You Think It Is

You will hear professional investors (such as Private Equity people) talk about “Total Addressable Market” (or TAM). This is the number of potential customers that fit your Target Customer Profile within the geographic range that you cover. You will also hear them talk about “The Law of Large Numbers.”

This “law” says, if the TAM is big enough, even winning a small percentage of it will enable the company to attain the goals of its Value Creation Strategy. Professional investors tend to like this condition - since getting a smaller market share is easier and more likely than getting a larger one - thus the investment is more likely to succeed. Let’s find out if your TAM can support your value creation goals as a Managed Services Provider (MSP), and whether there’s room in the market for everyone.

Contents

The Law of Large Numbers and SMB Managed Services

What follows applies to all markets worldwide, though our previous article about TAM, in our Q1-2018 newsletter, “When and How to Open a 2nd, 3rd, 5th or 10th Office,” used the Louisville, KY metropolitan area1 as our example.

-

The U.S. Census Bureau’s updated data says that in the Louisville metro area, there are 1.29mm people. More importantly for our purposes, there are 2,354 firms (companies) with between 26 and 100 employees; the typical target “SMB” size range and therefore our Target Customer Profile (TCP).

-

These companies employ a total of 83,836 people, or an average of about 35 employees.

-

From our own experience, we know that, worldwide and in any given target customer size, about 25% of CEOs think about IT in such a way that they will get into a win/win relationship with you for IT Services. That is, about 25% of decision-makers in any given customer size, anywhere in the world:

- Have critical IT needs,

- Know they have critical IT needs,

- Want to delegate those needs to someone outside their company, and

- Have the means and are willing to pay a win/win price.

- Therefore, of these 2,354 firms, we can safely assume about 25% or 588 firms, will buy the “full meal” Managed Services deal.

- The average price for a fully managed environment coming from an Operational Maturity Level™ (OML™) 4 MSP focusing on the SMB space2, is about $175 per employee. Therefore, the OML 4 MSP gets about 35 x $175 x 12 months = $73,500 in Annual Recurring Revenue for each deal they close.

- To this, the OML 4 MSP will cross-sell about $38,000 in product (including cloud resale) and about $17,000 in projects per year, for a total per SMB customer of about $128,500.

- Therefore, the TAM for an OML 4 MSP in Louisville is about 588 customers times about $128,500 or about $75,000,000.

It’s important to note that the other 75% of firms in the 26-100 employee size range will spend about the same amount - $75,000,000 – on IT. However, the higher growth, higher profit and better differentiated OML 4 MSPs will ignore these companies. The reason why is self-evident: each of these firms spends about 1/3 as much per year on IT ($75,00,000 divided by 1,766 firms).

That alone would make them unprofitable to do business with. Include in the equation that these firms tend to be more price sensitive, want to buy more on an a la carte basis, cross-shop product and Service providers and want to weigh in on IT operating decisions more often, and you can see why MSPs who are focusing on a win/win relationship, avoid them.

We now see that the TAM in Louisville is $75,000,000. How does the Law of Large Numbers factor into this? It already has, to a significant degree:

- We have narrowed our focus from all companies in the Louisville metro area (of which there are 22,522 according to the Census Bureau) to just the 2,354 that are in the 26-100 employee (i.e. SMB) space,

- We have further narrowed our focus on just 25% of those SMB companies.

A prudent investment analysis, however, would consider we will only win a fraction of even that narrowed population. Let’s say, then, of 25% of companies in the 26-100 employee space, we win only 15%. That is, only 15% of the 588 “win/win” style customers:

- We would have 88 customers,

- Who together would generate about $11,000,000 in Revenue,

- Including about $500k in MRR.

We have won only 88 customers. That’s only 3.7% of the companies in Louisville with between 26 and 100 employees. That’s only 4/10th of a percent of the 22,522 companies in the Louisville metro area. Therefore, we can be comfortable the Law of Large Numbers applies to this investment analysis.

Reality Checking Our Value Creation Strategy Versus Our TAM

Let’s say that our value creation goal is to create a company that can be sold for $10mm. Can we do that in Louisville, pursuing SMB customers? Or, do we need to add or move to another market and/or pursue larger (or smaller) customers?

We now know if we’re in the Louisville market, we can safely conclude that with a strenuous but accomplishable piece of work, we can build an $11mm SMB-focused Managed Services firm. Because we’re at OML 4, we’re charging about $175/user/month, getting our share of the product and projects (i.e. all of it) and we’re at Best-in-Class (top quartile) profitability – about 18.5% adjusted EBITDA3.

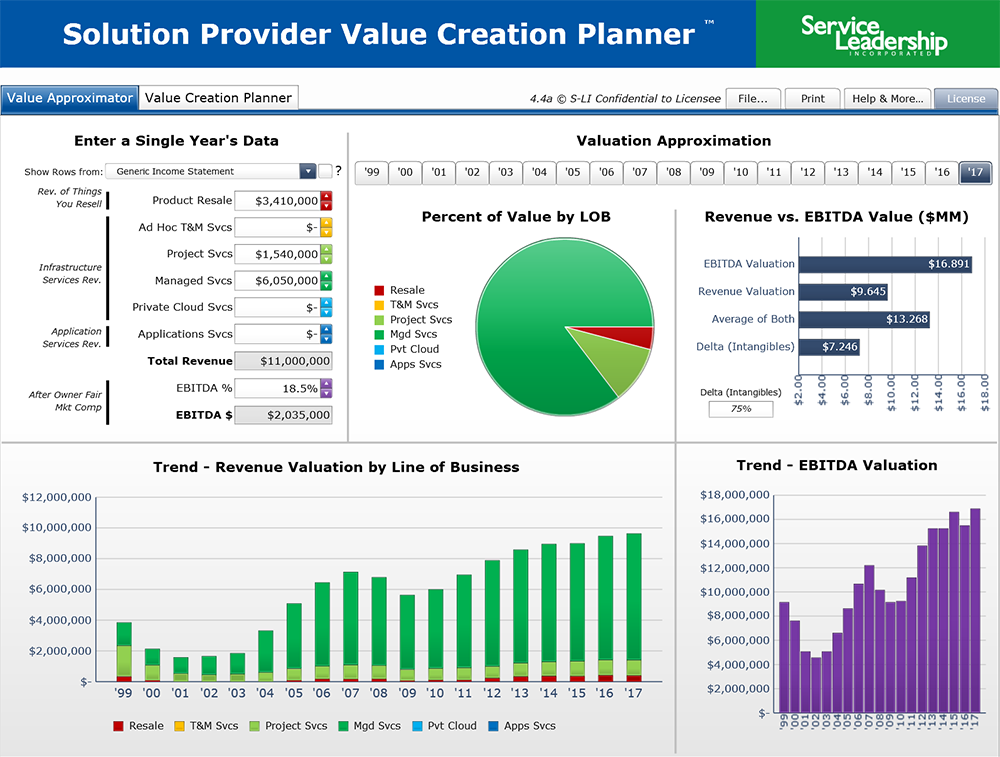

What would be the value of my company, having won the 88th customer? We can’t predict the valuation multiples in the future, but we can extend 2017 valuation multiples4 forward to play “What if?” Those of you who subscribe to SLIQ™, our Operational Maturity Level improvement app5, have access to our exclusive Solution Provider Value Creation Planner™ tool. It helps you plan your value creation approach in 5-year increments.

Here’s what it says about our Louisville scenario:

Our $11mm MSP is generating about $2mm in adjusted EBITDA – an attractive asset indeed, in today’s market. The valuation summary is in the bar chart in the upper right corner. Using 2017 multiples as a very simple, rough and approximate method of valuation, we can see that, on an EBITDA basis, the firm might be valued at nearly $17mm and on a Revenue valuation, perhaps about $9.6mm. The average of these two approximate valuations is, then, about $13.2mm. Using the TAM and Law of Large Numbers methods employed by professional investors, we can reasonably conclude we can attain our Value Creation Strategy of $10mm in stock value.

But is five years a reasonable time frame?

Let’s say that, today, we’re an average SMB MSP. That means:

- We are at about OML 3.4.

- We have about $4.5mm in total Revenue, generating 8.5% adjusted EBITDA.

- We have about 76 material customers, some 70% of whom are in our TCP of 26-100 employees (the rest are either above or below our TCP). Thus, about 53 of our current 76 material customers, are in our TCP and are therefore likely to be keepers.

- We won’t fire the non-TCP customers; we’ll just let them leave of their own accord over time, while we focus on getting more customers in our TCP, and especially the 25% of them who have the “win/win” IT decision-making style.

- We have one sales rep.

Based on this, the Solution Provider Value Creation Planner tool in SLIQ tells us our current stock value is about $3.1mm. Can we get to our goal of $10mm in value in five years?

We know we need year 5 to be $11mm in Revenue, which means 88 TCP customers versus our current 53 TCP customers. That’s about 2.4 times higher Revenue, but only about 1.7 times as many material customers, all within our TCP. We also need to be at Best-in-Class Adjusted EBITDA % (that is, 18.5%) not the median 8.5% we’re at today.

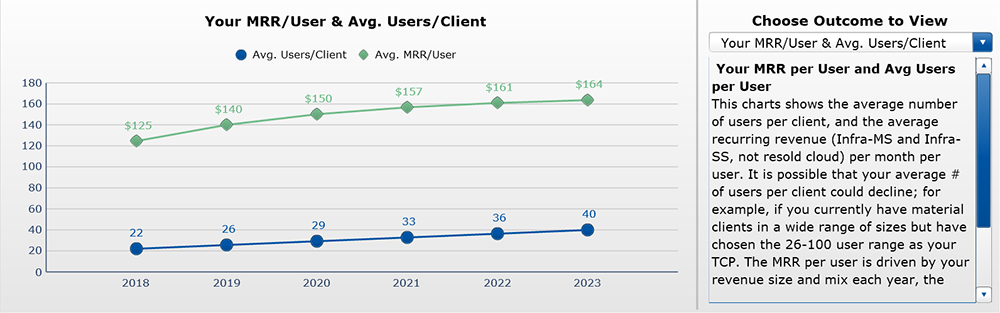

Clearly, we’re going to need to raise prices. Today we’re at about $125/user/month plus product and projects. The OML 4 MSPs are, as we’ve seen, at about $175/user/month plus product and projects. Today, our average customer within TCP has about 22 users. We’re going to need to get that to about 40 users.

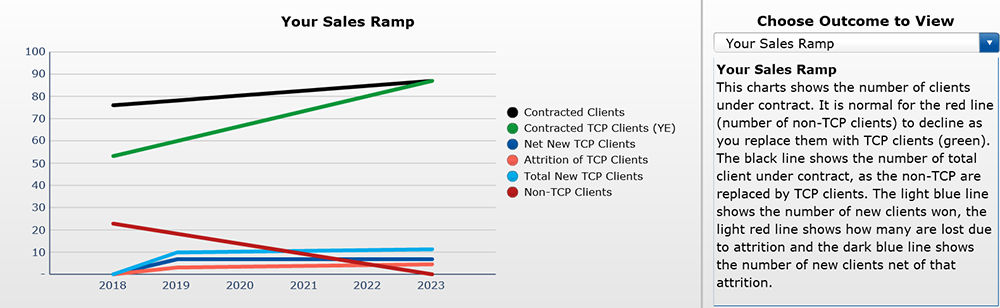

The Solution Provider Value Creation Planner in SLIQ tells us this will have to be our five-year sales ramp, if we’re going to hit that $13.2mm in value:

The green line shows the number of in-TCP accounts we will have to have to attain our value creation goal. How reasonable is this ramp?

Well, we have one Sales person today. A solid SMB Managed Services Sales rep, with good self-lead generation, supported by good marketing, can close about 1 deal per month. If we assume that we add a second Sales rep along the way, the Solution Provider Value Creation Planner in SLIQ tells us the pair of them should be able to get us where we need to be, in five years:

The chart tells us that each sales rep basically needs to close one deal a month – slightly less actually – for us to attain 88 TCP customers (and taking into account reasonably low customer attrition) in five years. That seems doable if we work hard at it.

What do we need to accomplish in terms of average customer size and fee/user/month? The Solution Provider Value Creation Planner in SLIQ tells us we do indeed need to raise our average users-per-account from 22 to 40 users – without any one account exceeding our 100-user TCP top end. That seems doable if we work hard at it.

It also tells us we need to get our average fee/user/month from our current OML 3.4 pricing of about $125 to $164, not quite to OML 4 levels.

We know the OML 4-ish folks are accomplishing substantially this in every market. So, we’re going to have to sharpen our lead generation – indeed turn it into demand generation. We’re going to have to sharpen our expression of value – probably by becoming more vertically focused at least to some degree and possibly exclusively. We know we’re going to have to get even more disciplined about selling the “full-meal deal” and about cross-selling everything we do to every one of our customers. That does seem doable if we work hard at it.

This Value Creation Strategy seems viable. We know we’re going to work hard anyway, so we might as well do it the high OML way.

Note, however, it ends year 5 with $13.2mm in value. While that would be wonderful, our goal was $10mm.

Adjusting the Solution Provider Value Creation Planner downward from $13.2mm to a $10mm stock value goal, we find our fifth-year Revenue needs to be just below $10mm (not $11mm) and the number of win/win, TCP customers needs to be 66 not 88. This means that, including reasonable account attrition, each of our two Sales reps needs to close only about six deals a year, not 10 or 11.

We’ll take the $10mm as our most-likely case, and set $13.2mm as our stretch goal.

How Many SMB MSPs Can the Market Sustain?

Because our best data is about the U.S., we’ll focus there. The ratios we have been using, can be applied reasonably safely to other countries, as well.

If we look at the 26-100 employee TCP across the 917 metropolitan and micropolitan areas tracked by the U.S. Census Bureau, and apply the same ratios noted above, we believe the TAM for SMB Managed Services in the U.S. is about $50bb, including recurring Revenue, product resale, and project Revenue. For example:

- Take the top 20 metro areas in the U.S.,

- Narrow that to just SMBs between 26 and 100 employees,

- Narrow that to just the 25% who will engage in a win/win Managed Services relationship,

- Figure that 80% of these will in fact do so,

- The result will be $4.4bb in Revenue for SMB Managed Service Providers (MSPs). That’s 440, $10mm MSPs, or an average of 22 per market.

- The next 20 markets add another $2.1bb.

- There are 877 more, albeit smaller, metro- and micro-politan areas to go. Put another way, the SMB MSP TAM, is huge.

The $50bb nationwide, is from win/win customers – the 25% of SMB companies that want your fully-managed package and will pay a fair price for it.

There is probably another $50bb available from the 75% of SMB companies who will only engage in a win/lose arrangement (and whom you should ignore). As we have discussed, MSPs at higher OML focus solely on these win/win customers and only on selling their fully-managed package; these are key reasons they grow the fastest and have the highest profitability.

With $50bb in TAM and if every MSP attains $10mm in Revenue, then there is “room” in the U.S. for about 5,000 well-performing MSPs of that size. There are probably about 15,000 MSPs in the U.S. today. The majority are well under $10mm in Revenue; in fact, the majority are under $5mm in Revenue.

It’s unlikely that sub-$10mm MSPs (or even sub-$1mm MSPs) will disappear completely. It’s even less likely that, in 20 years’ time, there will be only, say, 500 SMB MSPs each averaging $100mm in Revenue. But it is likely there won’t be 15,000 SMB MSPs.

Managed Services are similar to other professional Services –physicians, accountants, attorneys-at-law and so on – in important aspects of how they are sold, managed and delivered. For the same reasons there are not just a few large accounting firms or law firms, Best-in-Class SMB Managed Services will always have thousands of providers.

As we noted above, the TAM for SMB Managed Services, is huge. Additionally, we fearlessly predict that:

- We are five or so years away from the fee/user/month peak in the SMB MSP business,

- The number of SMB companies (i.e. potential customers) will expand,

- As will their understanding of and demand for, high-value IT operations.

Yes, in five years’ time, in 10 years, in 20 years, you’ll be offering a much-evolved array of Services, but smart customers will still be relying on thousands of MSPs – or whatever they’ll be called at the time – to help advise on and operate their digital existence.