So, what does this tell us? That the M&A market for MSPs — for all types of Solution Providers in fact — is very active right now. But, before you jump on the "selling my business" or "buy a business" bandwagon, you first need to understand what your stock value is, what it needs to be, and determine how to get that value.

What Drives Value?

There are several factors that drive value:

- Geography: This is more often luck, than anything else. If you’re located where the prospective Buyers have a gap in their map, you may be worth relatively more.

- Customer relationships: Strong customer relationships which the Buyer can leverage immediately. They’re looking for deep and broad, not "Managed Services a la carte" or run rate product fulfillment.

- For Product-Centric firms, vendor/solution focus: Buyers look to add capabilities around certain technology vendors for two reasons: (1) to develop a greater market position with a given vendor; and (2) to secure more expertise in selling solutions and services around technology stack.

- For MSPs, vertical focus: Educated Buyers know that higher performing MSPs tend to be focus on at most, two or three verticals, and not generalists. This is because the customer relationship is stronger when you know more about their industry, and you can better generate leads and close deals when you’re part of the prospect’s professional community.

- For Product-Centric firms, profitable, quality infrastructure projects services: It’s critical to have service-led product sales, as opposed to product-led service sales.

- Also, for Product-Centric firms, at least some credible Managed Services: Value can be driven up materially by being able to show that you not only design and sell the client a solution including the technology stack (product or products) and implementation (project), but also monitor and manage it for them on a recurring revenue basis. Even if this revenue stream isn’t large, having demonstrated ability to sell a sequence of Managed Services contracts helps the Buyer feel comfortable your team has at least initial capability to sell more. It may be more expertise than the Buyer’s own team has, in selling and delivering Managed Services.

- Top quartile financial performance: The foundation for most valuation methods is performance at generating cash flow, typically approximated by Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA). Both the size of the pile of EBITDA dollars, and the EBITDA percent are important. It is harder for Buyers to find companies with a large amount of EBITDA dollars, which benefits many Buyers’ need to deploy as much cash as possible. And it’s difficult to find one with a higher EBITDA percent, which provides the Buyer with greater safety in several ways. The same is true for consistent growth.

This leads us to valuation multiples.

Valuation Multiples are High

The good news is that multiples are high. In fact, they are higher than they were in the previous market peak of 2007.

So, why are multiples high?

The primary reason is what is almost always behind high valuation multiples: Outsiders with lots of money coming into the market and buying Solution Providers. This is coming from two directions, both happily coming at the same time for completely unrelated reasons.

The lesser trigger was Konica-Minolta’s purchasing of All Covered for a high multiple, and then tearing across the U.S. buying sizable SMB MSPs at unprecedented multiples and cash-heavy deal structures. This is a smart thing to do, for a major corporation with billions a year to invest. They (and now Ricoh who bought mindSHIFT) see erosion of their traditional copier customer base to the digital world, and want a part of that world.

This high profile buying binge left many smaller MSPs feeling passed over: "If I was only twice my size, they would have picked me." Hence, MSPs buying MSPs, driving multiples up.

The larger trigger was, paradoxically, the cloud. The transition of tens of thousands of hourly break/fix IT services companies to the more scalable model of Managed Services, should have attracted well-heeled outside buyers to consolidate the industry. It didn’t, because no-one outside the IT services business really knows what Managed Services is, nor are there any larger vendors or "research" firms touting Managed Services to Wall Street.

When the IT vendors decided that cloud was this decade’s "paradigm shift in computing" and started touting it to Wall Street as such, Wall Street started noticing that the "last mile" to small and medium business to sell the cloud, is controlled by MSPs (not by the cloud vendors).

As a result, while Venture Capitalists (VCs) pour money into cloud startups, their equally well-heeled cousins, the Private Equity Groups (PEGs) have been ramping up their interest and investments in consolidating MSPs. This drives multiples up. It also drives up existing MSPs’ desire to be bigger, to appeal to the PEGs. This further drives up multiples.

Thus, while the cloud vendors and "research" analysts mistakenly shout "fire in the channel," they miss that they’re not only factually wrong but also that cloud is creating more demand for good MSPs among well-heeled investors and buyers.

It’s perhaps humorous that many VCs mistakenly believe their cloud startups can "disintermediate" the channel, while the PEGs are betting heavily the channel is cloud providers’ only successful route to market.

We could ask the more experienced cloud vendors. Microsoft has learned the hard way that customers want their Solution Provider involved. Adobe, which has effectively transitioned much of its business to the cloud, has its largest-ever channel community. Salesforce.com has a thriving channel community. Perhaps the PEGs are right?

How long will the conditions driving high multiples last? Who knows? Our bet is, as long as the vendors keep touting cloud to Wall Street, a material portion of PEGs will figure out that the channel is cloud’s best route to market, and that MSPs are the most scalable part of the channel.

How Likely Are You to Get High Multiples?

If you’re a larger MSP, you’re going to be more attractive to a buyer seeking scale. In 2016, the average MSP was about $4.7mm in revenue. About 85% of Solution Providers are under $10mm in revenue, so exceeding $10mm is likely a good thing because such companies are hard to find.

If you’re an MSP or Product-Centric firm in the top quartile of profitability for your business model (buy our S-L Index™ Annual Solution Provider Industry Profitability Report, here), you’re going to be more attractive to a buyer. By definition, those in the top quartile of profitability make up only 25% of the MSP and Product-Centric population, which is good thing because they’re hard to find. Being hard to find, when you’re at or near top quartile profitability, means you can command higher multiples.

Now, if your revenue is over $10mm and you’re in the top quartile profitability, you are likely to be extremely attractive.

Higher profitability companies are also less risky for the buyer: More cash flow to pay off the money spent making the acquisition, and more room to make operational mistakes post-acquisition.

On the flip side, the smaller your business, and the lower in profit performance, the lower the multiple you are likely to earn, and the less attractive you are likely to be.

How Much Do I Really Need?

This is where it gets tricky. Let’s say you’re an average MSP, that is, about $5mm in revenue. If you talk to a professional financial planner, they will tell you that for every $40,000 a year you want in passive income, you need to have invested about $1mm in the typical array of stocks, bonds and similar assets.

So, if you want to have, say, $160,000 a year in passive income — which you can enjoy and live off of while you go fishing, do volunteer work or start another company — you need to have invested about $4mm.

To obtain this $4mm of investable dollars from the sale of your MSP, depends on a number of conditions, of which the multiple is only one.

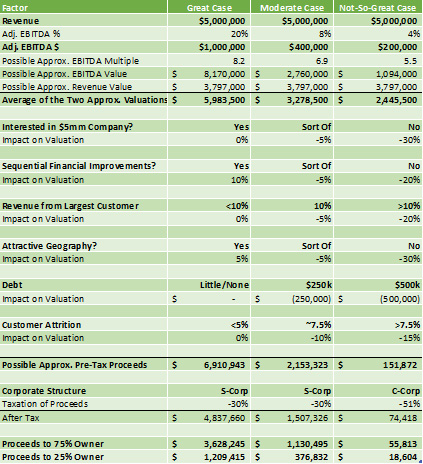

What Does a $6mm Valuation Look Like? And What Gets in the Way?

To make it simple. Let’s assume you have built a $5mm MSP operating at Best-in-Class EBITDA of around 20%. This would give you EBITDA of about $1mm.

At current EBITDA multiples, taken in isolation, this would mean a stock value of around $8mm.

If your revenue mix was right, the revenue multiples would put you in at about $3.7mm.

Averaged together, this would put your valuation at about $5.9mm.

Call it $6mm for round numbers. That is, if:

- You can get someone interested at that about-average size,

- You are showing sequential improvements in growth and profitability over time,

- You don’t have much more than 5% or so of your revenue coming from your largest customer,

- You’re in a geography attractive to the buyer,

- You don’t have a lot of debt,

- You don’t have a lot of customer attrition,

- You’re willing to agree not just to the value, but to the deal structure (basically, the amount of cash up front versus on contingency) they’re offering,

- And so on.

Now, let’s see what else we find in our path to getting $4mm in investable cash.

It is important to note that we are not financial planners, CPAs (or chartered accountants) nor are we attorneys-at-law. You should check everything we say with your licensed professional advisors before making or acting on any decisions.

- Corporate structure: If you’re what is called in the U.S. a "C-corporation," you are likely headed for double-taxation on your proceeds of the sale, once at the corporate income level and once at the personal income level. If you’re an "S-corporation," limited liability corporation or similar, you will be taxed only once. So, there’s either about 60% off the top, or 30%.

- Number of owners: Across the entire Service Leadership Index®, the number of owners in the average IT Solution Provider is 2.1 people1. Thus, whatever you sell the company for, it will presumably be split between them. Let’s assume one owner has 75%, and the other owner (we’ll ignore the 0.1 owner) has 25%.

- Debt on the Balance Sheet: Ironically, debt often has the effect of driving up the purchase price, making the company less attractive to the buyer, and perhaps the deal less do-able even if the buyer remained interested. Debt drives up the purchase price because the seller has a take-away number in mind. If the debt — which typically must be paid off when the company is sold — drives down the take-away cash, the seller won’t do the deal unless the buyer increases their offer.

There are other factors, but let’s just work with these, and with the bullets above them.

Three Financial Outcomes: Great, Moderate and Not-So-Great

Note that everything in the following table is our opinion — granted an educated one. Any given Solution Provider will likely have different outcomes.