Executive Summary: The State of Product-Centric Partners

The VAR/Reseller Business Model Based on Partners’ Own Normalized Financial Data

Introduction

Product-Centric firms in the Top Quartile of profitability for the business model, produce a higher bottom-line profit percentage than do Services-Centric firms who are performing at Median for any of their nine business models.

The Service Leadership Index® is the largest scale, longest-running and most detailed benchmark subscribed to by Solution Providers worldwide. Each year since 2008, we update the S-L Index™ Annual Solution Provider Industry Profitability Report™, the leading comprehensive sourcebook for Solution Provider owners and vendor channel executives seeking empirical data about the financial and operational performance of Solution Providers in 10 business models, segmented by Top Quartile, Median and Bottom Quartile performance.

This executive summary previews some of the exclusive data on Product-Centric Solution Providers – that is, VARs/Resellers – to be published in the 2019 S-L Index Annual Solution Provider Industry Profitability Report later this year.

Contents

“VAR” is Not a Four-Letter Word

The Service Leadership Index objectively categorizes all Solution Providers (globally and across all sizes and segments) based on their Revenue mix, into one of 10 Predominant Business Models™ (PBMs™):

- Product-Centric;

- Five distinct Infrastructure-Services-Centric business models; and,

- Four distinct Applications-Services-Centric business models.

This is because each of the 10 PBMs responds to different best practices and has different financial performance potential (more on this,

here) as well as different potential stock value. They also have different needs when seeking to add or optimize the different possible lines of Services business.

Increasing the proportion of Services Revenue (growing Services Revenue faster than Product Revenue), usually results in lower profit performance, unless specific best practices are followed for measuring and optimizing Services profitability in a Product-Centric firm.

Product-Centric firms are those Solution Providers with at least 60% of their top line Revenue (not gross profit) coming from reselling hardware and software, including cloud resale. This Predominant Business Model™ (PBM™) responds most productively to “Services-Led” rather than Services-Centric best practices. (Firms with more than 40% of their Revenue coming from their own Services, fall into one of the nine Services-Centric PBMs.)

Product-Centric firms in the Top Quartile of profitability for that PBM, produce a higher bottom-line profit percentage than do any of the nine Services-Centric firms who are performing at Median profitability for their PBM.

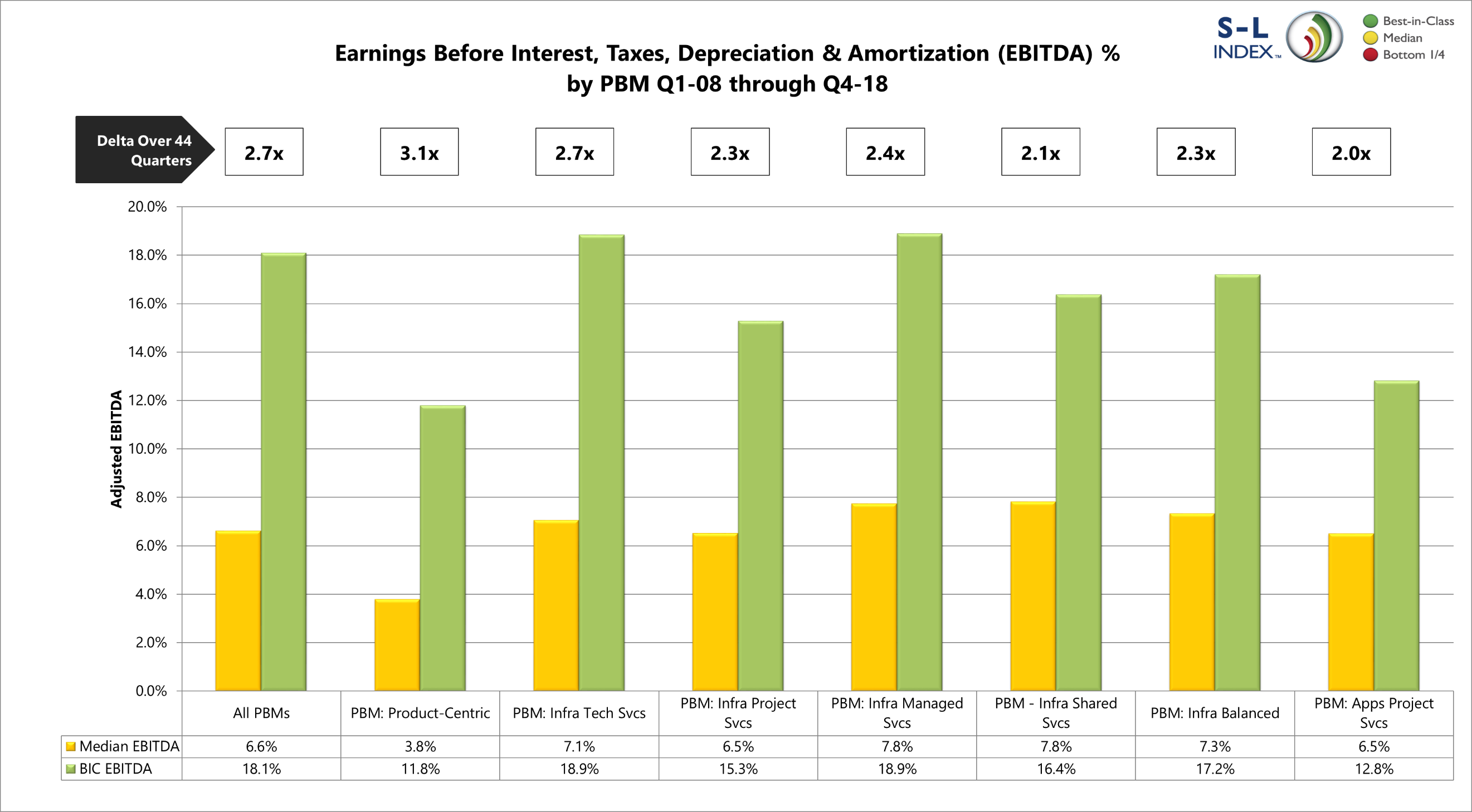

The chart above, compares the Top Quartile by EBITDA1 profitability (Best-in-Class or “BIC”) and Median profitability firms in various PBMs over the past 44 quarters.

As you can see, over the past 11 years, one-quarter of Product-Centric firms (shown as a green bar) had bottom-line profitability of 11.8%. In contrast, Services-Centric firms at median profit performance for their PBM, do not exceed 7.8% bottom line. Size for size, the BIC Product-Centric firms deliver at least 60% more profit dollars to their shareholders than do the Median Services-Centric firms.

In round numbers, the Product-Centric firm, if it runs at BIC profitability for its PBM, delivers something like 1,100% more profit dollars to its shareholders, than does the Services-Centric firm running at Median profitability for its PBM.

This difference is even more material given that the average Product-Centric firm has about six times higher top-line Revenue than the average Services-Centric firm.

This means, in round numbers, the Median-sized Product-Centric firm, if it runs at BIC profitability for its PBM, delivers something like 1,100% more profit dollars to its shareholders, than does the Median-sized Services-Centric firm running at Median profitability for its PBM.

Stock values of privately-held Solution Providers are typically based at least partially on EBITDA dollar production, which puts the Best-in-Class-performing Product-Centric firms in a good light. That said, business model – Services Revenue and especially recurring Services Revenue – also typically plays a large role in valuation.

Those Product-Centric firms who have the highest stock value, have done so by successfully becoming “Services-Led” yet deliberately not becoming fully Services-Centric. However, merely increasing the proportion of Services Revenue (that is, growing Services Revenue faster than product resale Revenue) alone, usually results in lower profit performance, unless specific best practices are followed for measuring and optimizing Services profitability in a Product-Centric firm.

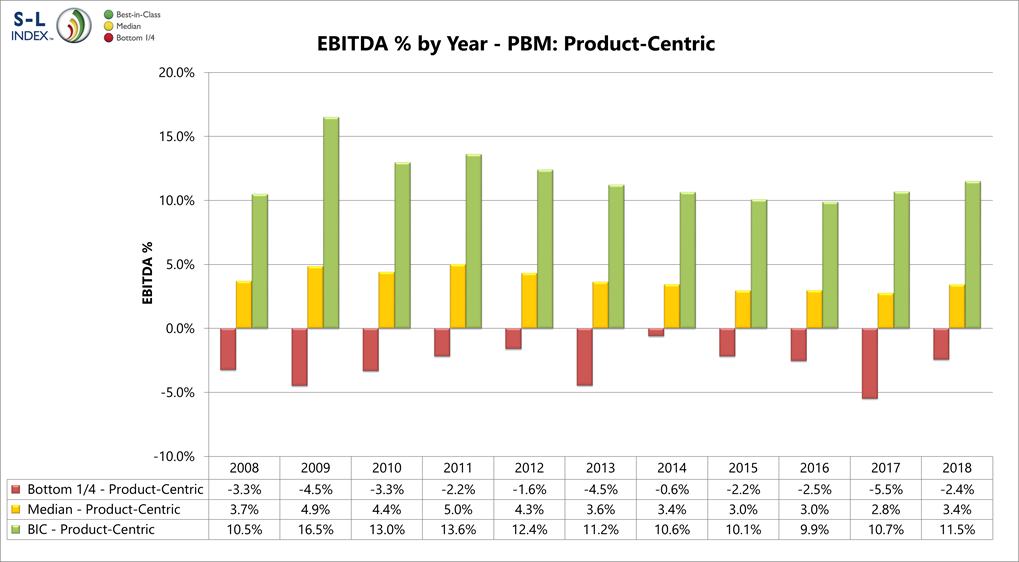

Best-in-Class VARs’ Profit Trends Up for the Second Year Running

Coming into 2017, even the Best-in-Class Product-Centric firms had declined in bottom-line profitability for five successive years. This is an indication of how challenging the resale-plus-Services model is. There are a number of reasons for this, but suffice to say, even these high Operational Maturity Level™ (OML™) management teams lost ground five years in a row.

Happily, by the end of 2017, these top performers had broken this unfortunate streak and posted slightly higher profitability than in 2016. We are pleased to announce here, that 2018 results show Top Quartile profitability for Product-Centric firms, rose again last year. As the chart below shows, the Top Quartile in this business model in 2018, attained 11.5% EBITDA after fair market owner compensation.

This performance by the Top Quartile Product-Centric companies, is their highest since 2012. We congratulate the Product-Centric management teams who are in this Top Quartile of Adjusted EBITDA % in 2018.

Even more exciting: In 2018, for the first time since 2011, the Median-performing Product-Centric firms were finally able to deliver an increase in profitability, turning around seven successive years of decline. In addition, the Bottom Quartile were able to halve their losses in percentage terms. Together, these results show not only improving economic conditions but also the incrementally higher Operational Maturity Levels™ (OMLs™) of the Product-Centric community. More on the OMLs of Solution Provider companies and the specific best practices for increasing OML in each of the Solution Provider business models, in our 2019 S-L Index Annual Solution Provider Industry Profitability Report.

We should note that, should the economy veer into a recession, the higher-OML management teams of the BIC firms typically show the greatest ability to defy broader economic trends. Those of the Bottom Quartile, having lower OML, typically show the least ability to buck the down-trends, and their results most closely mirror the broader economy.

Stark Differences in Successful Revenue Mix Transformation

The Best-in-Class Product-Centric firms are indeed successfully becoming Services-Led. These high-OML firms use methods that are either not known or not pursued by the lower-OML firms who try to increase the proportion of Services with less effective methods, which damage the firm’s profitability. As a result, the high-OML firms are safely and productively growing Services Revenue faster than Product Revenue, successfully becoming more Services-Led, while the lower-OML firms time-and-again retreat from Services as their bottom lines degrade.

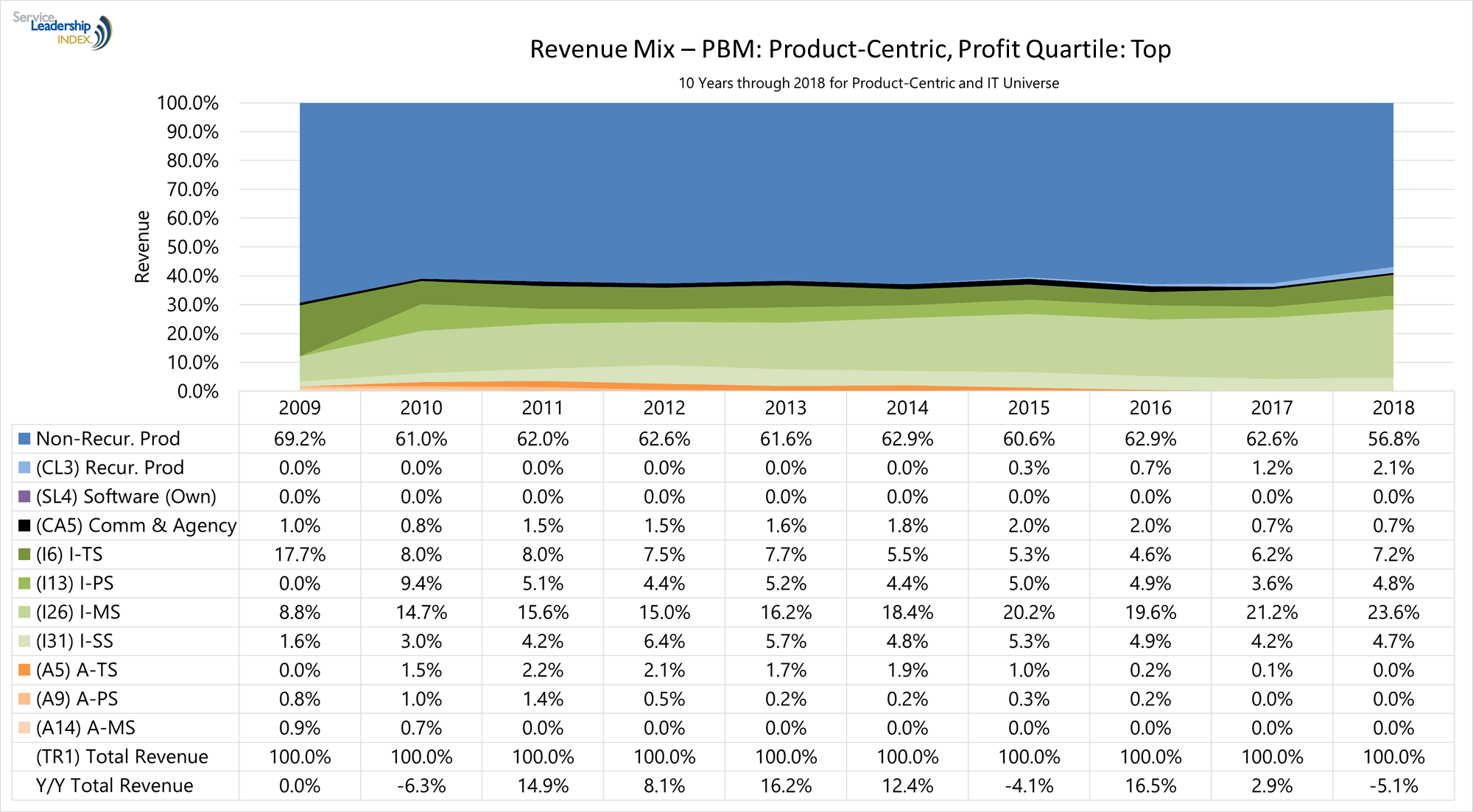

The first chart below shows the change in Revenue mix of the Product-Centric firms in the Top Quartile of profitability for their business model in 2018.

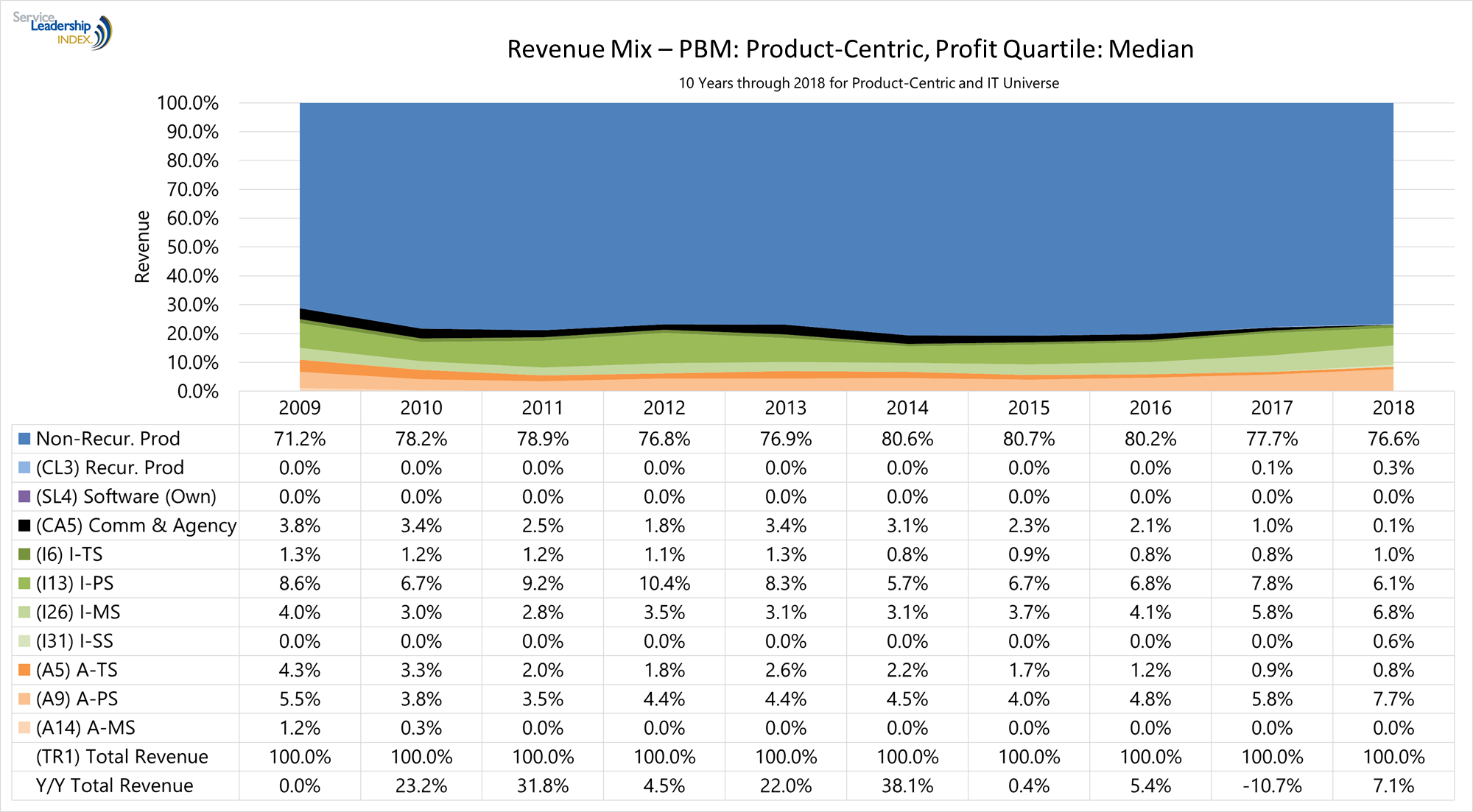

The next chart shows the Median profitability firms in the same business model.

Recall that the top profitability firms – while effectively the same average size as the Median firms – have about 3.1 times higher EBITDA profit percent. They have taken the steps to sell Services profitably (which also enables the Services to be of higher quality and differentiation). The Median firms have effectively not grown the proportion of their Revenue from Services at all.

It is critical to note that they frequently try to do so. However, they fail to apply the best practices specific to improving Services profitability in a Product-Centric company, so as Services Revenue grows, bottom line profit drops. They then retreat from Services growth, typically laying off Services people to stem losses, with the concomitant decline in Services Revenue.

It is how Service and Product are sold and delivered, that separates the Product-Centric companies who are in the Top Quartile – that is, who are successfully Services-Led – compared to those who, as they add services, reduce their profitability. For example, here are just three of the roughly two-dozen behavioral differences exhibited by the top performers:

- Top performers correctly categorize pre-sale engineering and unbilled labor hours in Services cost, not Sales cost or general and administrative expenses (G&A). This produces behavior changes in strategy, Sales and Service which favor greater Services “attach,” lower Services Cost of Goods Sold (COGS), higher Service delivery quality and accelerated sales cycle, outcomes which also produce higher product gross profit production.

- Seemingly paradoxically, top performers also narrow the range of products for which they commit to providing implementation, support and Managed Services. This drives up margin, quality, sales enthusiasm for service, customer value and referrals and, as a result, profitable Revenue growth.

- Top performers pay Sales people on actual Services Gross Margin, not imputed or guaranteed Services margin, recognizing that while Service is responsible for as-delivered margins, Sales has a material influence on it as well, both before and after the sale.

As a result of these and the other best practices evidenced by the top-performing (that is, successfully Services-Led) Product-Centric firms, their ability to drive added value to their clients while operating more efficiently, enables them to earn higher Gross Margins in most practices and on product resale.

Stock Value Winners: VARs or MSPs?

The common assumption is that Product-Centric firms do not generate increased stock value as effectively as Managed Services Providers (MSPs) or what we call Infrastructure-Managed Services-Centric firms.

As part of our services, we have monitored the stock value multiples of Revenue and EBITDA in private transactions into which we have visibility in the Solution Provider marketplace, each year since 1999. We then apply those multiples to the benchmark results of our clients, to provide them with an approximation of their stock value each year.

Because the Service Leadership Index is the longest-running and largest-scale benchmark of Solution Providers, we can provide unparalleled views of both short- and long-term trends.

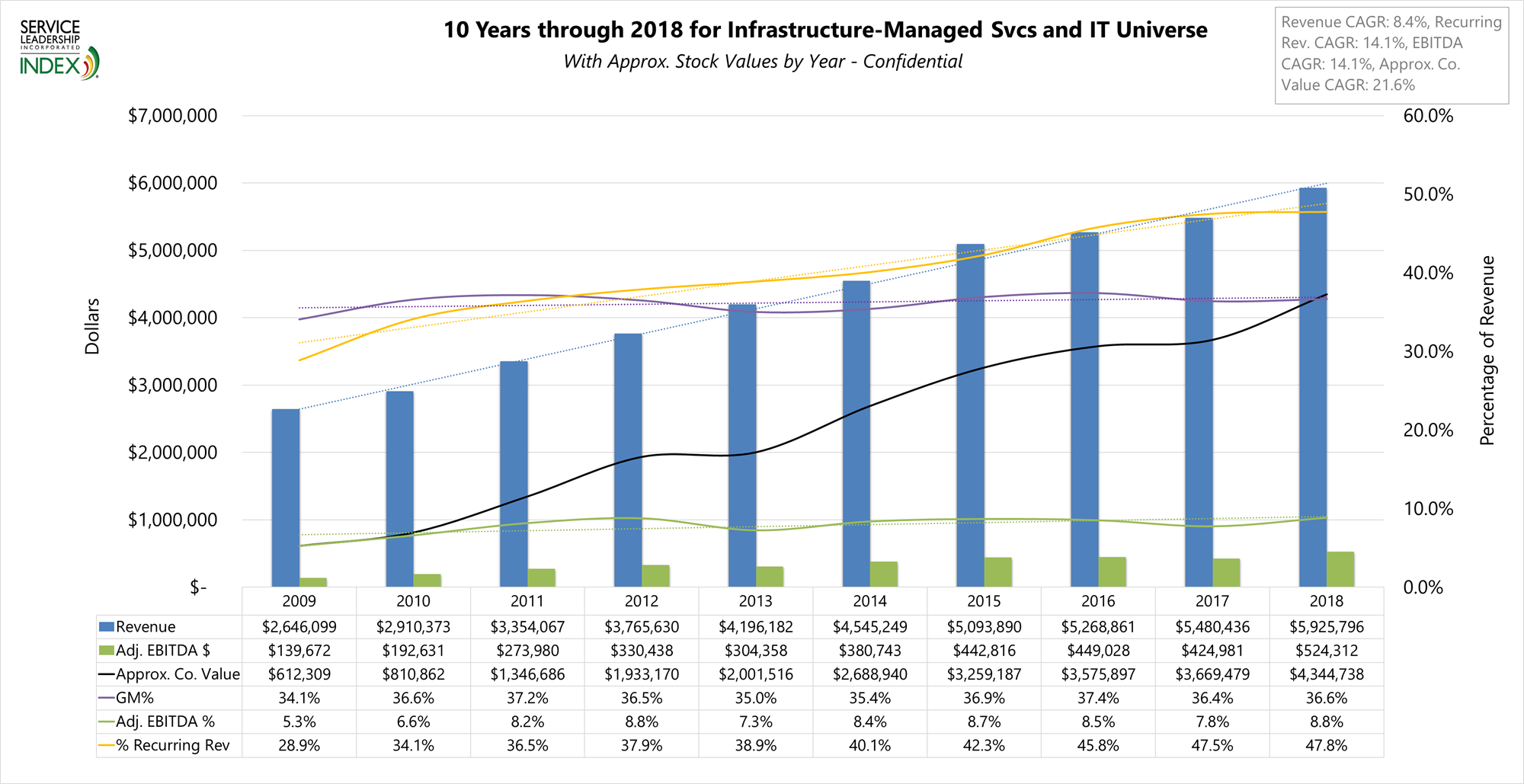

The first chart below shows the stock value creation performance of MSPs in the Median profitability group for their PBM.

This performance is certainly impressive. As the box in the upper right notes, these MSPs – most of whom are focused on Small and Medium Business (SMB) customers – have grown their top-line Revenue at a rate of 8.4% compounded annually.

Most impressively, they were able to increase their stock value a stellar 21.6% compounded annually over the 10-year time frame. This is a result of multiple factors:

- Favorable movements in valuation multiples over this time, and

- These MSPs drove a steadily increasing the proportion of recurring Revenue, and

- They also drove up EBITDA percent while they grew Revenue, resulting in 14.1% compound annual growth in EBITDA dollar production.

Since EBITDA dollars and recurring Revenue dollars are among the most influential of the 15 value creation drivers for Solution Providers, these MSPs earned impressive gains in stock value even though they were “only” in the Median profitability group. The Best-in-Class MSPs did even better.

While owning a business is always risky, short of correctly picking high-flying public stocks over 10 years’ time, this exceptional increase in value is difficult to attain any other way.

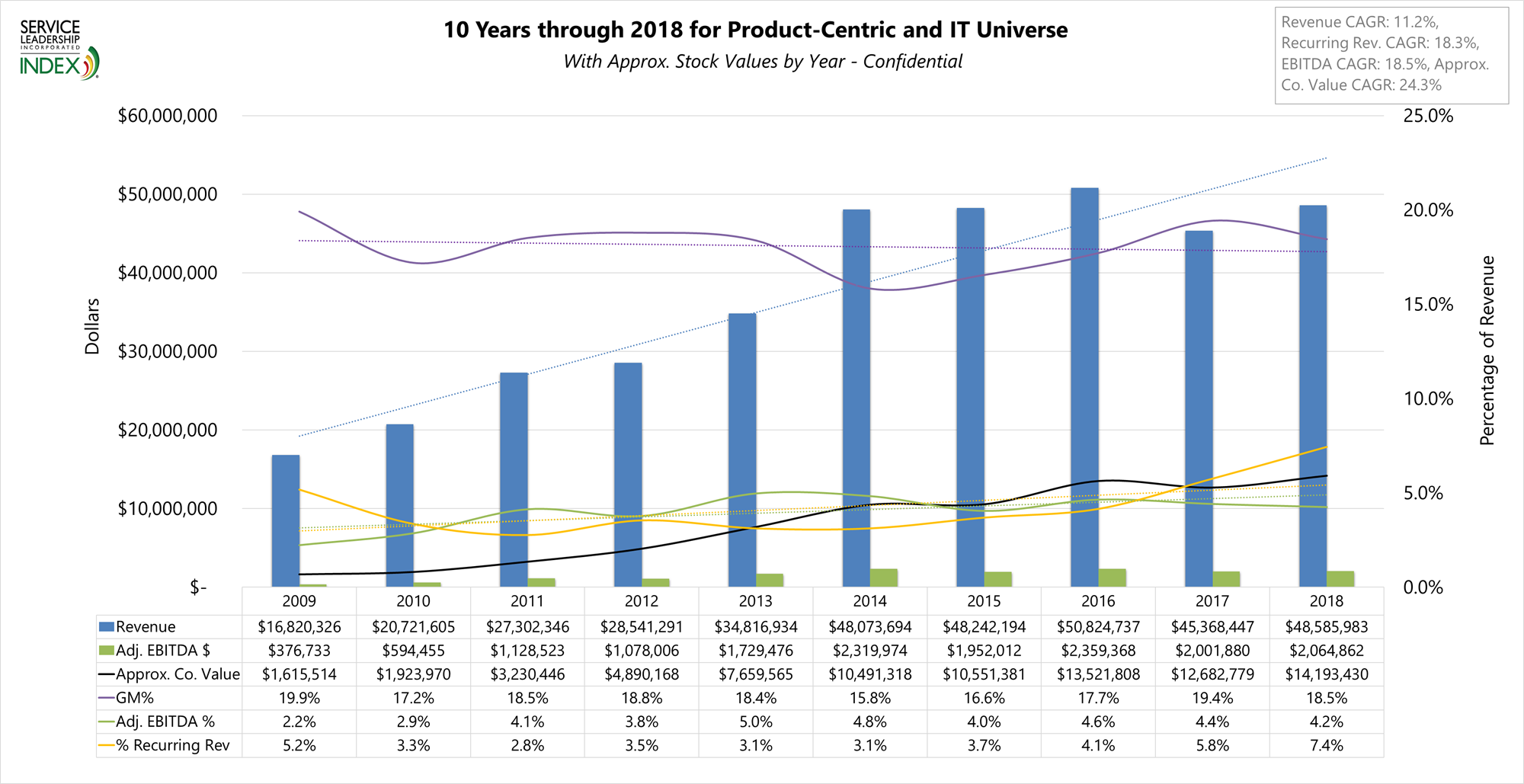

However, as the chart below shows, the Median Product-Centric firms performed even better over the same time frame.

Here, we can see that the Median Product-Centric firms earned compounded annual growth in stock value of 24.3% versus 21.6% for MSPs.

In each of the value creation growth metrics, the Median VARs – who largely target mid-market and enterprise customers, not SMBs – handily beat their SMB MSP peers:

| Value Creation Factor |

SMB MSPs |

Mid/Enterprise VARs |

| Top-Line Revenue Growth ($) |

8.4% CAGR |

11.2% CAGR |

| Recurring Revenue Growth ($) |

14.1% CAGR |

18.3% CAGR |

| EBITDA Growth ($) |

14.1% CAGR |

18.5% CAGR |

| Approx. Company Value Growth ($) |

21.6% CAGR |

24.3% CAGR |

While still solidly Product-Centric, they have managed to drive improved value creation results faster than their SMB MSP peers.

The 24.3% compound annual growth rate in stock value is a result of several factors:

- As with the SMB MSPs, firms in the Product-Centric business model benefited from the upward draft in valuation multiples over this timeframe.

- However, the greater gains came from improvements in their own performance:

- They tripled their Revenue,

- At the same time doubling their Adjusted EBITDA %,

- Resulting in an increase in their EBITDA dollar production in 2018 of nearly 5.5 times greater than in 2009.

- While their proportion of recurring Revenue only increased from 5.2% to 7.4%, because of their overall Revenue increase, the absolute gain in recurring Revenue dollars – which currently earns the highest Revenue multiple when valuing Solution Providers – was just over four times (about $873,600 in recurring Revenue in 2009 versus about $3.59mm in 2018). While still a small part of their business, relative to its size it’s valuable; a dollar of recurring Revenue currently is about ten times more valuable than a dollar of Product Resale Revenue.

But it was the 5.5 times increase in EBITDA dollars which drove the outstanding value creation performance. Depending on the size of the pile of EBITDA dollars, a dollar of EBITDA profit is worth about 46 times as much as a dollar of Product Resale Revenue. The old advice is sometimes the best: fix the profit model first, then grow.

In seeking to drive performance even faster, and to safely and productively get to a more Services-Led (but still Product-Centric) business model, these Median Product-Centric firms should take another look at the best practices used by the Best-in-Class in their business model, three of which are noted above in this executive summary, and more of which are discussed here.

We’ll leave you with one more of these best practices: the top performers in the Product-Centric business model, focus not only their Product Resale and Project Services businesses on mid-market and enterprise customers, they also focus their Managed Services on these larger customers. Lower performers in the Product-Centric business model, mistakenly try to do SMB Managed Services while serving mid-market and larger customers with products and project services.

We congratulate Product-Centric firms in all profit quartiles for improved results in 2018, and for their outstanding stock value creation over the past 10 years.